WEEK 6 -

VIABILITY and REFINEMENT with a SOUPçON of SOM

Three Key Characteristics of a Minimum Viable Product

It has enough value that people are willing to use it or buy it initially.

It demonstrates enough future benefit to retain early adopters.

It provides a feedback loop to guide future development.

1. Uniqueness

Before you worry about upstart financing, marketing or business location, you should begin with an idea—not just any idea, but one that's unique. What makes your business stand out from the rest? Uniqueness doesn't necessarily mean you have to invent something (though that's never bad—just look at Snuggie's success), it just means that you have to set yourself apart from the competition. If you're starting a catering company, say, what will make your catering service different from the rest? These are tough questions, but important ones. The most successful businesses have a strong, unique concept, and a clear identity. Take the time to define yours.

2. Upstart Funds

What will your start-up cost be? Every business has some expenses at the start, whether you're paying for equipment, rent or just basic marketing materials. Make a realistic estimation; you'll need these figures to obtain a loan or simply to budget if you're paying these expenses out of pocket.

3. Customer

Who's your customer? Knowing who will be buying your product or service is vital to your business success—how else will you find your customers if you don't know who they are? Are you catering to busy professionals, stay-at-home moms, college students, retirees? Define your customer, even if you have to be broad at first. If you'll be renting a space, make sure the local demographic fits this profile; the real estate agent will be able to provide you with that data.

4. Competition

Unless you're lucky enough to find a hole in the market, your business will have competitors. Check them out, because your future customers surely will. Competitors can be a great resource to you as an upstart; you can see how much they charge, what marketing strategy they use and the location they chose. Ask yourself: how can I do better than the competition? Use your uniqueness identified in step one to find ways to outdo your competitors.

5. Economic Mood

Your business' success can greatly depend on economic mood: imagine starting a luxury real estate business at the start of the housing crisis. Gauge the state of the economy, and think of how it relates to your upstart: where are consumers' mind right now? Are they cutting back, spending more time at home, concerned about the environment? Even an economic downturn can be an opportunity if you can meet the mood of the consumer. If your business idea doesn't fit the current trends in spending, think of ways you can tweak it to tap into today's needs.

6. Timing

Timing is crucial, especially for an upstart. Opening an ice-cream shop in January is a bad idea; opening Memorial Day can make it the place to be that summer. Do you expect your business to be seasonal? If so, time your opening to the strongest consumer demand. You'll come out of the gates with a flood of new customers, customers who will come back for more.

7. Marketing

Remember step three, where you identified your customer? Now you have to develop a marketing strategy to make sure these potential buyers know about your great new business. With today's internet capacity, marketing can be relatively low-cost, using online coupons and mailing lists. Brainstorm ideas with friends and family, and look at what your competitors do to get new business.

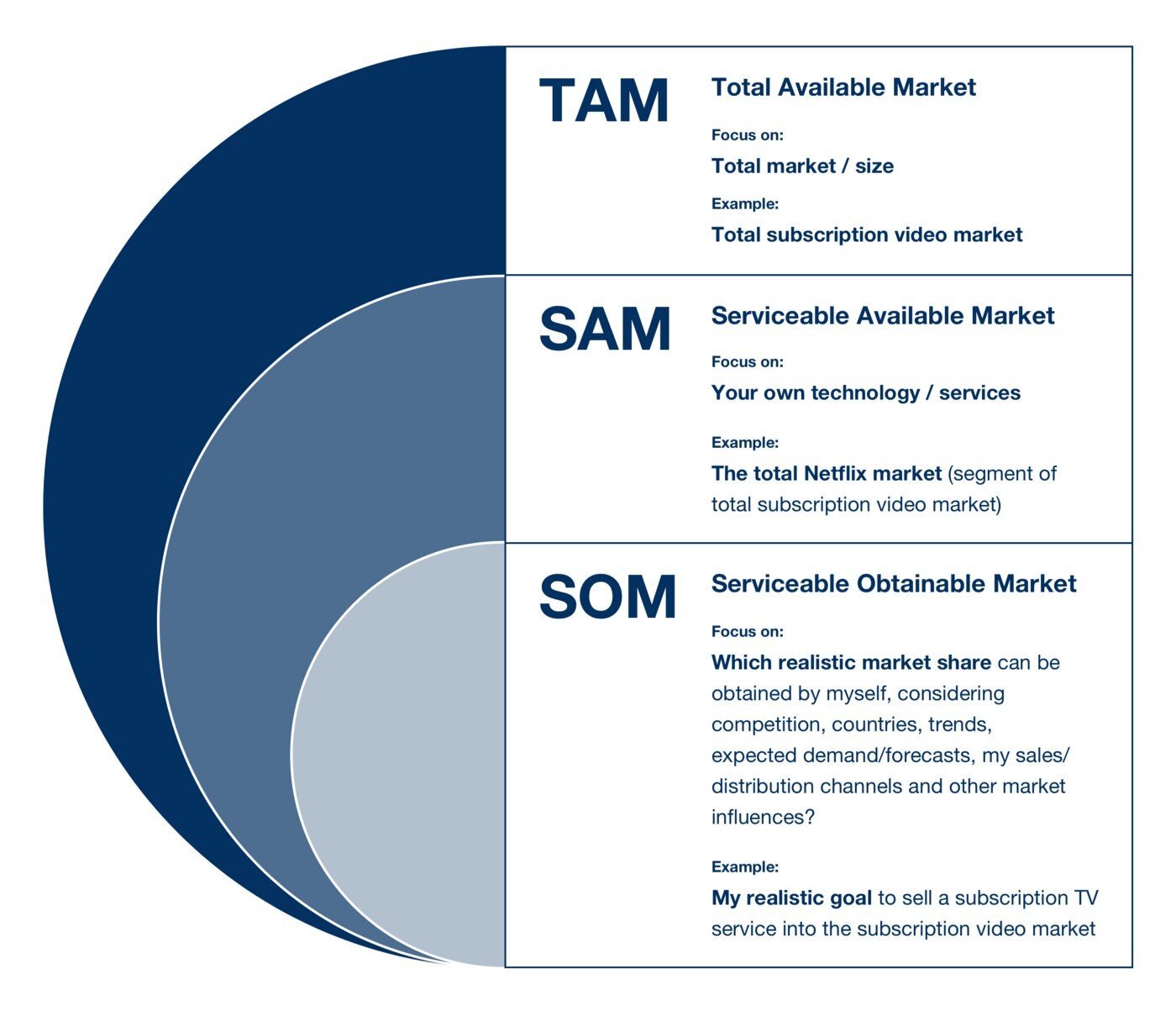

CALCULATING SOM/TAM USING A BOTTOM UP ANALYSIS

Bottom-up analysis First, find out how many customers are out there—often called “counting noses” because you have to get very specific about customers. This is done with primary market research techniques combined with some secondary market research, but dominated by the former.

Talk to as many people as possible in your end-user profile group. Find out from them how you can estimate the size. If it is a B2B business, find out how many there are in a few representative companies.

Then, determine the average density of your end-users in companies in your targeted area. This ratio (end users per 1,000 employees, or end users per $1M in revenue, or end users per product produced, or whatever is most appropriate in your situation) is an important metric that we can then extrapolate to the other companies, and build up your estimate in that way.

Collect and analyze source data (customer lists, trade associations, other sources of customer information) for things like lists of specific companies in the sector you are targeting. In the B2B example above, you can then estimate how many end users for each company name on the list. Company can be replaced with hospital, high school, region, fan club, or whatever is the most appropriate organizational unit for your project.

Make an estimate of how many potential users there are in the market. This is the first number that you need to know.

Next, come up with a valid range of how much revenue could be generated from an average single-target end user that fits your profile in the previous step. This is the amount of money they would spend in one year. If they buy your product which costs $100 once every five years, then the annual revenue for this is $100/5 years = $20/year. The more primary market research you can get to build the ratio for this number as well as the annual revenue per user (which can also be a range), the better.

Now calculate the bottom-up value of your TAM (number of customers × revenue per customer).

Place your TAM

ASSIGNMENT

VIABILITY STATEMENT PAPER

Address ALL points in the above breakdown to convince a group of investors that you have thought out this idea and have the data and roadmap to achieve product launch. This takes into account competition, funding potential and the ability to “bootstrap”.

Submit to CANVAS by 10/13/20